Iran War Update I: Oil at $100, Impact on the UK Economy, Russia Winning, and the Case for Energy Independence.

11 March 2026

Monday morning delivered a stark reminder of just how fragile the global economic order has become. Brent crude briefly breached $100 per barrel, a threshold that carries outsized psychological and economic weight, before retreating following a statement from President Trump suggesting the United States was close to achieving its military objectives and ahead of schedule. Markets exhaled. But the underlying conditions that drove oil to that level have not changed. If anything, they are deepening materially. llll

📈 The $100 Moment and What It Reveals

Oil at $100 is not simply an energy story. It is an inflation story, a cost-of-living story, and for the UK specifically, an interest rate story. The transmission mechanism is well understood: energy prices feed directly into transport, manufacturing, food production, and household bills. When oil spikes, inflation follows, and when inflation rises, the prospect of rate cuts diminishes. For a UK economy already contending with anaemic growth, incomplete post-pandemic recovery, and the structural friction of EU departure, a sustained move above $100 would represent a serious and potentially prolonged setback to the fragile stabilisation the Bank of England has been working toward.

Trump's intervention calmed markets on Monday, but it is worth being clear-eyed about what that calm represents. It is confidence in a statement, not confidence in a resolution. Crucially, the White House has confirmed it has no timeline for when the Strait will be safe for commercial shipping again, a significant admission that the operational reality lags far behind the political messaging. And even if and when the Strait does reopen, the backlog of trapped vessels — the Gulf is currently packed with tankers unable to exit, with Iraq already cutting production to just 1.3 million barrels per day as it runs out of storage — means that oil held up in the region will take weeks, if not months, to transit, refine, and reach consumers. The physical supply chain does not respond to press conferences.

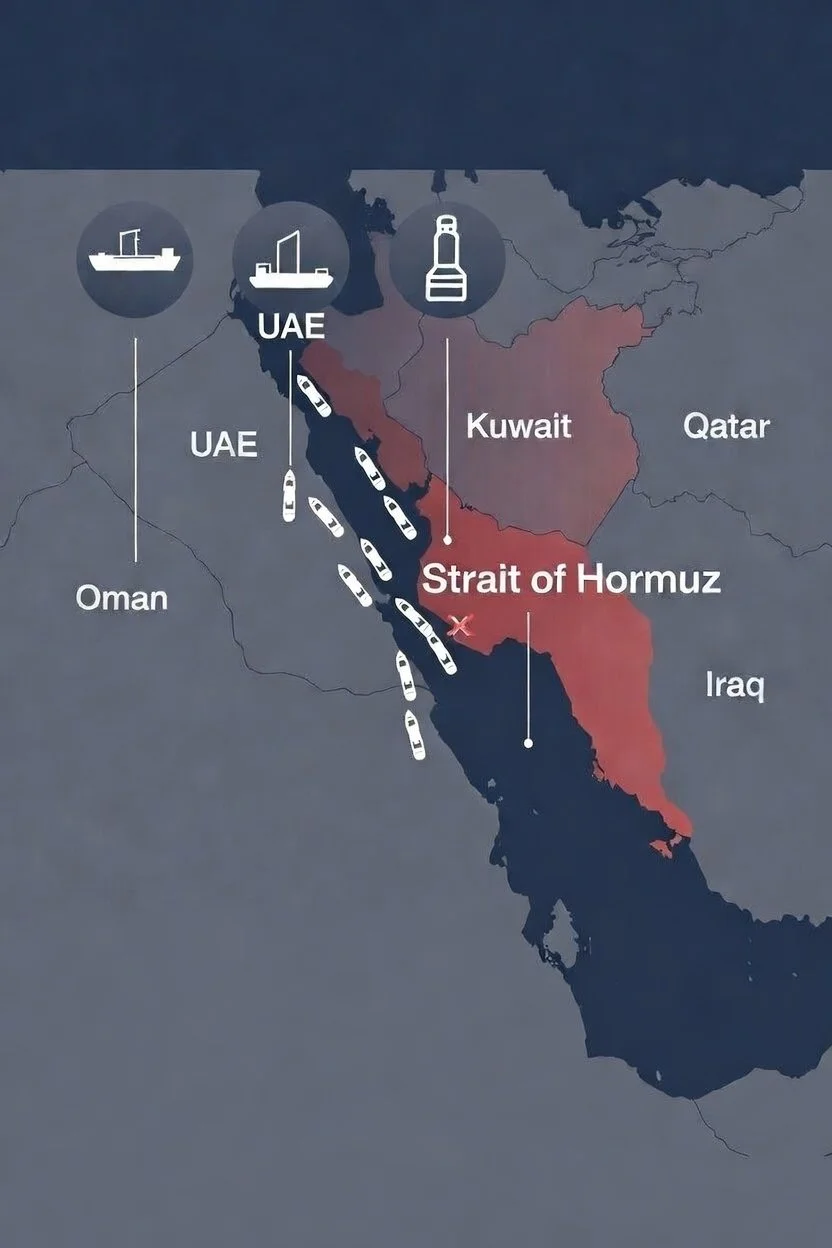

⚠️ Mines in the Strait: Escalation in Real Time

Since Monday's brief reprieve, the situation has materially worsened. Iran has begun laying naval mines in the Strait of Hormuz, with the IRGC estimated to retain the vast majority of its mine-laying capability still in reserve. Iran's inventory is estimated to include between 2,000to 6,000 naval mines, according to estimates, a figure that renders the current deployment the opening move in a potentially prolonged campaign of physical obstruction, not its conclusion. Naval mines represent a qualitatively different threat to the Strait than missile attacks or vessel seizures. They are persistent, time-consuming and technically demanding to clear, and they introduce a degree of physical, not merely political, risk to every vessel considering transit.

A military solution to opening the Strait is not yet feasible as the US Navy has so far declined requests to escort tankers due to “high risk”. The only realistic path to a material return of transits requires shipowners to be convinced that the route is safe for their crew and vessel assets, a condition that is nowhere near being met. The parallel with the Red Sea crisis is instructive but limited: the Red Sea is an open chokepoint that ships can bypass via the Cape of Good Hope. Hormuz is closed. There is no alternative route for the crude, LNG, and petroleum products bottled inside the Persian Gulf.

🛢️ The G7 Reserves Response: Reassurance, Not Resolution

On 10 March, G7 finance ministers issued a joint statement declaring their collective readiness to “take necessary measures” including a coordinated release of strategic oil reserves, with the announcement serving as an immediate psychological stabiliser for markets that had seen Brent briefly touch $119 per barrel. The intervention is significant but it must be understood for what it is and, crucially, what it is not.

The statement was primarily a market confidence measure. The physical reality is considerably more complicated. Strategic reserves hold crude oil, not refined products, and not all crude is equal, the Gulf primarily exports medium-sour crude, which not all refineries can process, meaning even a large release may not fully replace the type of oil that is actually missing. Critically, oil prices react the moment a reserve release is announced, before a single barrel hits the market, meaning the price relief seen this week is running ahead of any actual supply improvement. Once the market recognises that gap, volatility will return.

🌾 Beyond Oil: The Fertiliser and Food Security Shock

The Strait of Hormuz is not only an oil and gas chokepoint, and this dimension of the crisis has received far less attention than it warrants. Around 30% of internationally traded urea , the most widely used nitrogen fertiliser, passes through the Strait, along with significant volumes of ammonia and sulphur used in phosphate fertilisers.

For UK farmers specifically, only about 40% of the nitrogen fertiliser required is produced domestically. The fertiliser shock translates into higher food production costs with a lag, and ultimately into higher prices on supermarket shelves, adding yet another inflationary channel to an already pressured consumer environment.

🇷🇺 Russia: The Conflict's Quiet Beneficiary

While Western attention is focused on the Gulf, Russia is the party benefiting most from the current disorder, and doing so without firing a shot in this particular theatre. With Gulf supply constrained and Qatar's LNG suspended, energy-hungry economies across Western Europe and Asia face renewed pressure to secure alternative supplies. Russia, despite sanctions, remains one of the few actors with the production capacity and pipeline infrastructure to fill that gap at scale. Every day the Strait remains disrupted, Russia's leverage grows. It can offer supply to countries that need it, at prices that reflect scarcity, on terms that incrementally rebuild its economic and political relationships, precisely the relationships that sanctions were designed to sever. The conflict in the Gulf is, from Moscow's perspective, an extraordinarily convenient development.

🏠 The UK Mortgage Market: Echoes of 2022

The conflict is now transmitting directly into the UK mortgage market in ways that will be felt by millions of households. Average two-year fixed mortgage rates have risen above 5% as nearly 500 mortgage products have been pulled off the shelves in the last two days, with lenders withdrawing products as swap rates surge in response to repriced inflation expectations. Before the conflict, markets were pricing an 80% probability of a Bank of England base rate cut on 19 March 2026. The picture has changed quite substantially now. The comparisons to the September 2022 mini-budget under Liz Truss are being made widely across the industry, and they are not without foundation. This is shaping up to be the biggest mortgage market shock since the 2022 mini-budget, with swap rates climbing sharply and entire product ranges being taken down. The mechanism is different, then it was fiscal credibility; now it is an exogenous energy shock, but the market behaviour is recognisably similar: rapid repricing, product withdrawal, and borrowers facing a deteriorating landscape with little warning. For the 1.6 million UK mortgages expected to expire in 2026, many of which were fixed at pandemic-era rates, the timing could scarcely be worse.

📉 The UK's Compounding Exposure

The economic implications for the UK are multi-layered and mutually reinforcing and they land on an economy uniquely ill-placed to absorb them. The accumulated weight of structural vulnerabilities, anaemic growth since 2008, incomplete pandemic recovery, and the friction of EU departure, has left the economy's buffers depleted in a way that is largely without parallel among comparable developed nations. The OBR's recently published forecast that inflation would fall sustainably below 2% must now be called into serious question. The path to 2% does not run through an energy shock, a fertiliser crisis, a mined maritime chokepoint, and a destabilised mortgage market simultaneously. Rate cuts recede. And a Treasury that had quietly been counting on lower borrowing costs to underpin its fiscal projections faces a materially harder path.

🌍 The Case for Energy Independence

The lesson being written in real time is that energy and food dependency are not merely economic vulnerabilities, they are strategic ones. Diversification of supply sources is insufficient: moving from Russian gas to Gulf LNG simply replaced one vulnerability with another. The only durable answer is a genuine reduction in import dependency, through accelerated domestic energy production where viable, and a serious, economically credible transition to renewable energy at scale. This is a national resilience argument, not an environmental one. Countries that generate a significant share of their own energy are insulated from precisely the kind of shocks now recurring with increasing frequency.

🏦 Key Considerations for Banks and Financial Institutions

The current crisis carries direct and material implications for banks' capital planning frameworks. Under PRA supervisory rules, most UK firms are required to update their Internal Capital Adequacy Assessment Process (ICAAP) at least annually, and critically, more frequently in the event of a material change in circumstance. The events of the past ten days almost certainly meet that threshold.

Banks should be actively considering the following within their ICAAP stress scenarios over the next twelve months: a sustained oil price above $100 and the inflationary second-round effects on credit quality across consumer, mortgage, and corporate portfolios; the repricing of energy-exposed sectors including petrochemicals, agriculture, shipping, and logistics; elevated counterparty risk in trade finance and commodity-linked exposures; the impact of a structurally higher-for-longer interest rate environment on loan impairments and net interest margin projections; rising mortgage arrears risk as fixed-rate deals expire into a materially higher rate environment; and concentration risk in any portfolio with significant exposure to Gulf-region counterparties or supply chains. Institutions with material exposure to shipping, energy, agricultural commodity, or residential mortgage sectors should consider whether an unscheduled ICAAP review is warranted in the near term. The PRA's expectation is clear: capital adequacy assessments must reflect the institution's actual risk environment. That environment has changed materially and rapidly.